In the grand theater of automotive decision-making, few dilemmas spark as much deliberation as the age-old question: lease or buy? This isn’t merely a financial quandary—it’s a psychological chess match where convenience, freedom, and long-term vision collide. The allure of driving a shiny new Toyota every few years, with its cutting-edge tech and warranty-backed reliability, whispers seductively to the modern consumer. Yet, the siren call of ownership—of planting roots in a vehicle, of eventually owning something outright—echoes just as loudly. The choice isn’t just about numbers; it’s about lifestyle, values, and the subtle art of balancing immediate gratification with future security.

For many, the decision hinges on a single, gut-wrenching observation: Why does the idea of driving a brand-new car every three years feel so exhilarating, yet so terrifying? The answer lies not just in the glossy brochures or the zero-percent financing ads, but in the deeper currents of human behavior—our love for novelty, our aversion to long-term commitment, and the quiet dread of obsolescence in a world that moves at breakneck speed. Let’s dissect this conundrum with the precision of a scalpel and the warmth of a fireside chat.

The Allure of the New: Why Leasing Feels Like a Victory

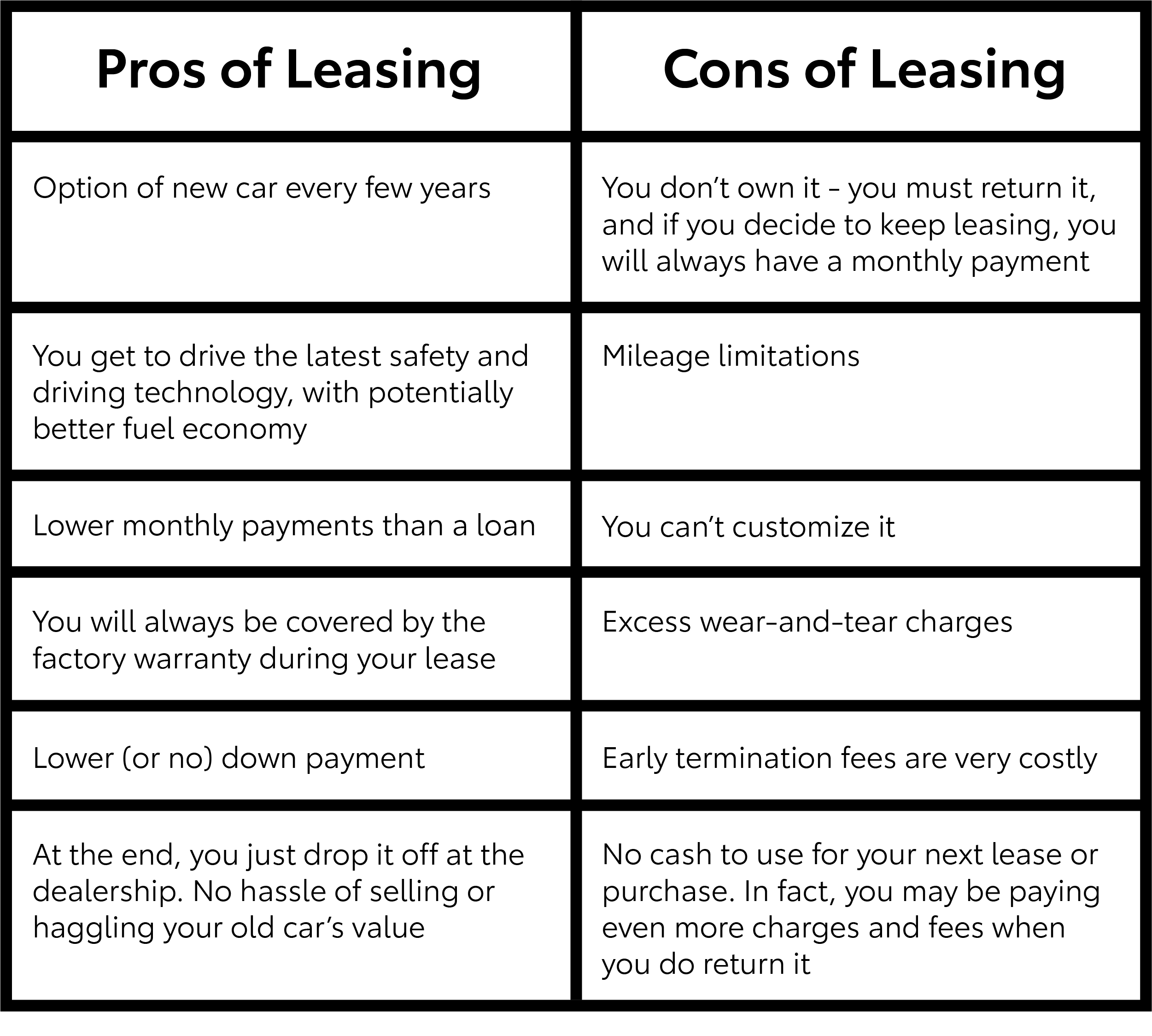

Leasing a Toyota is, at its core, an exercise in perpetual reinvention. Every two to three years, you step out of one vehicle and into another, as if shedding a skin that’s grown just slightly outdated. This isn’t just about transportation; it’s about curating an experience. The latest models bristle with features that didn’t exist a decade ago—adaptive cruise control that reads the road like a fortune-teller, infotainment systems that respond to your voice like a loyal butler, and safety suites that turn the car into a cocoon of protection. For the chronically curious, leasing is a backstage pass to automotive evolution.

There’s a psychological edge to this arrangement, too. The monthly payment, while not insignificant, is often lower than a loan payment for a comparable purchase. This frees up cash for other pursuits—perhaps a weekend getaway, a home renovation, or even another investment. The absence of long-term debt can feel liberating, like a bird released from a cage. Yet, this freedom comes with strings attached: mileage limits, wear-and-tear clauses, and the unspoken pressure to return the car in pristine condition. The exhilaration of driving something new is tempered by the knowledge that you’re, in essence, renting a lifestyle—and rentals, by definition, are temporary.

The Weight of Ownership: Why Buying is a Marathon, Not a Sprint

To buy a Toyota is to plant a flag. It’s a declaration: This is mine. This is where I’ll return, year after year, until the odometer hums with the stories of my life. There’s a permanence to ownership that leasing can’t replicate. With each payment, you’re not just servicing a debt; you’re building equity, a tangible asset that can be sold, traded, or gifted. The freedom to modify, to drive without counting miles, to let the car age like a fine wine—these are the perks of commitment.

Yet, ownership isn’t without its shadows. The initial sticker shock of a new Toyota can be jarring, even with financing. The depreciation curve is steepest in the first few years, meaning you’ll likely lose thousands the moment you drive off the lot. Maintenance costs, while lower in the early years, creep in as warranties expire. And then there’s the guilt of the unused features—the heated seats you never touch, the premium audio system that plays only to an empty cabin. Ownership demands patience, a virtue that’s increasingly rare in a world of instant gratification.

But here’s the deeper truth: buying a car is an act of rebellion against the disposable culture that defines so much of modern life. In a world where smartphones are upgraded every two years and fast fashion clogs landfills, a purchased Toyota is a defiant stand for longevity. It’s a statement that you value endurance over ephemerality, that you’re willing to endure the upfront cost for the sake of stability. The math may not always favor the buyer, but the soul often does.

The Hidden Costs: What the Ads Don’t Tell You

Beneath the glossy surface of lease vs. buy lies a labyrinth of hidden expenses, each capable of derailing even the most meticulous budget. Leasing, for instance, often requires a substantial down payment—sometimes as much as 20% of the car’s value—tucked away in a financial no-man’s-land where it earns no interest and serves no purpose beyond securing the deal. Then there’s the disposition fee, a cruel twist of the knife charged when you return the vehicle, as if the mere act of walking away incurs a penalty.

Buying isn’t immune to surprises either. Gap insurance, a necessity if the car is totaled before the loan is paid off, can add hundreds to the annual cost. Extended warranties, often pitched as a safety net, are little more than profit centers for dealerships, with payouts that rarely cover the full cost of repairs. And let’s not forget the opportunity cost: the money tied up in a car could have been invested, compounding over decades into a small fortune. The ads promise freedom, but the reality is a minefield of fine print.

The Emotional Equation: Which Choice Aligns With Your Soul?

Numbers tell one story, but emotions tell another. The lease-or-buy decision is, at its heart, a mirror held up to your values. Do you crave the thrill of the new, the ability to pivot without penalty? Leasing offers a symphony of flexibility, a way to dance with the future without committing to a single partner. It’s ideal for those who see cars as appliances—tools to be used and replaced, not cherished. The emotional payoff is in the variety, the constant upgrade, the absence of long-term ties.

Buying, on the other hand, is for the sentimentalists, the planners, the ones who see a car as more than metal and rubber. It’s for the parent who imagines teaching their child to drive in the same vehicle they once drove, for the road-tripper who wants to modify their ride without fear of voiding a lease agreement, for the pragmatist who believes in the power of compounding—whether in investments or in the miles they’ll drive over a decade. The emotional reward here isn’t in novelty, but in continuity. It’s the quiet pride of knowing you own something outright, something that’s yours to keep, to sell, or to pass down.

The Hybrid Approach: Can You Have Your Cake and Eat It Too?

Why choose between lease and buy when you can blend the two? The hybrid model—buying a lightly used Toyota and leasing a new one every few years—offers a middle path, though it requires a deft touch. By purchasing a two- or three-year-old model, you sidestep the steepest depreciation while still enjoying lower payments than a brand-new purchase. Then, when the lease on the new car comes due, you can either renew the lease, buy the used car outright, or trade up again. It’s a strategy that demands vigilance—tracking lease terms, resale values, and market trends—but for the disciplined, it can be the best of both worlds.

Another hybrid tactic is the “lease-to-own” arrangement, where a portion of your lease payments goes toward the eventual purchase of the vehicle. It’s a compromise that softens the blow of both options, though it rarely delivers the full benefits of either. Still, for those torn between the two, it’s a lifeline—a way to test the waters without diving headfirst into the deep end.

The Final Verdict: A Decision as Unique as You Are

There is no universal answer to the lease vs. buy dilemma. The right choice is the one that aligns with your financial reality, your lifestyle, and your emotional DNA. If you’re someone who thrives on change, who views a car as a temporary companion rather than a lifelong partner, leasing may be your calling. If you’re drawn to the idea of legacy, of building something that outlasts trends and fads, buying could be your destiny. And if you’re the type who likes to hedge their bets, the hybrid approach might just be the sweet spot.

One thing is certain: the fascination with this decision runs deeper than spreadsheets and interest rates. It’s a reflection of our collective unease with permanence in an impermanent world. We lease because we fear commitment; we buy because we crave roots. The Toyota in your driveway—or in your future driveway—isn’t just a machine. It’s a mirror.

So ask yourself: What do you see when you look in the mirror? The answer might just guide you to the right choice.