Compact cars have a particular kind of appeal: nimble handling in tight spaces, efficient fuel economy, and often an insurance profile that feels more forgiving than larger vehicles. Still, “compact” is not one single insurance category. Two drivers can buy the same class of car yet see dramatically different premiums once underwriting factors like safety technology, repair costs, claim frequency, garaging, and personal risk tolerance are pulled into the mix. What follows is a guided tour of compact car insurance costs—from lowest to highest—and the kinds of details readers should expect when comparing models, coverage styles, and real-world pricing behavior.

Think of compact car insurance as a spectrum. On one end sits the mechanically sensible, widely insurable vehicle—often paired with favorable crash-avoidance equipment and manageable parts pricing. On the other end lies the compact model that can be more expensive to repair or more frequently involved in costly claims. The gradient isn’t random; it’s shaped by data, engineering, and human driving patterns.

Understanding the compact car insurance “ladder”

Before mapping lowest to highest, it helps to clarify what “cost” means. Insurance quotes are not just about the car; they’re a braid of vehicle risk and driver profile. Even within compact segments, the “ladder” commonly reflects several forces:

Safety systems (automatic emergency braking, lane keeping, adaptive headlights) can reduce claim likelihood or severity. Repair complexity influences how quickly body shops can fix damage and how expensive parts become. Target demographics and usage can affect claim patterns; a model often chosen by commuters may show different loss behavior than one favored by younger drivers.

Most importantly, premiums change when coverage changes. Liability-only pricing tends to compress the range, while full coverage (comprehensive + collision) often widens it, especially in areas with higher theft rates, weather risk, or congestion-related incidents.

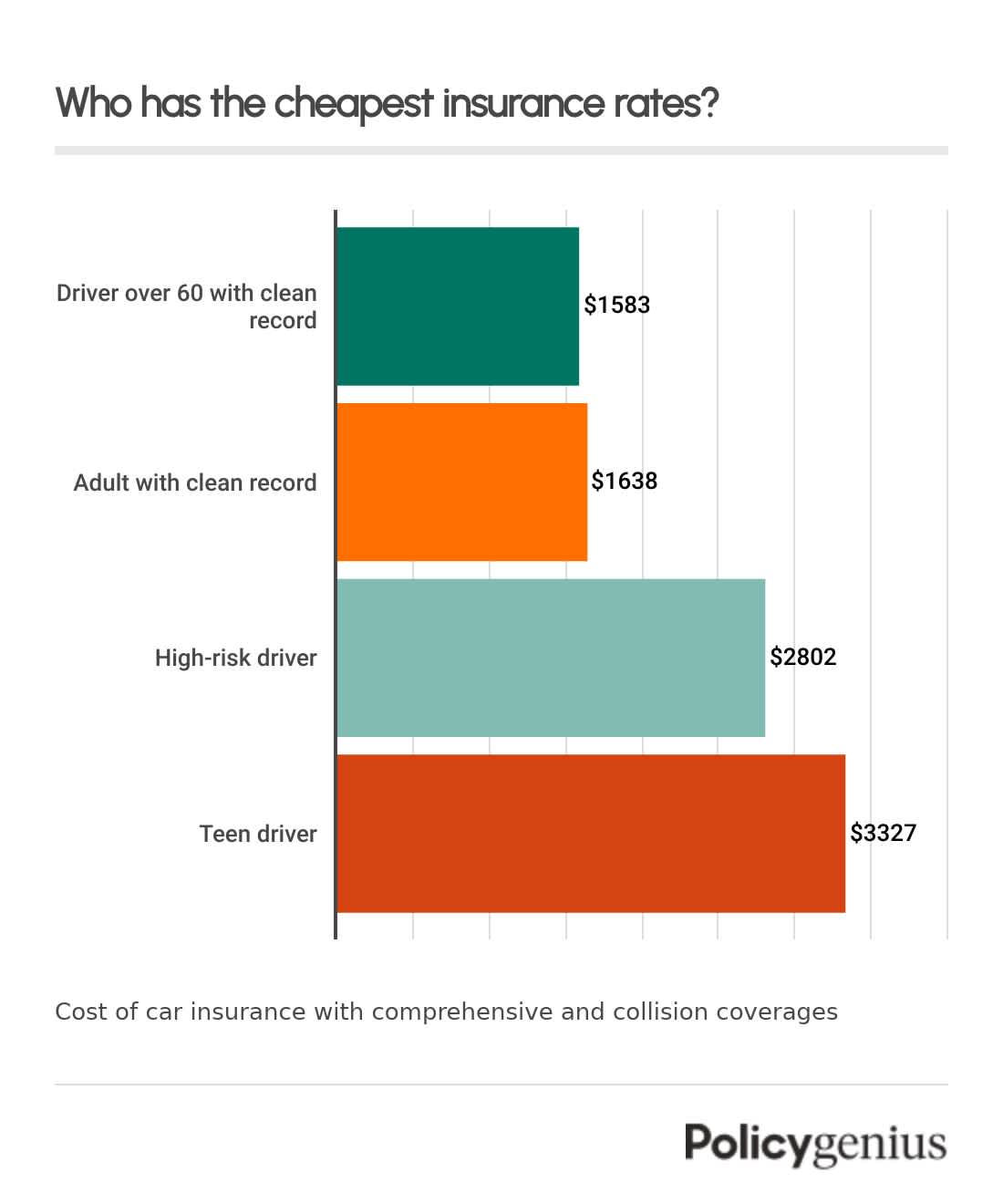

Lowest-cost compact car insurance: the “easy-to-insure” set

At the bottom of the spectrum are compact cars that tend to share a few traits: broad availability of parts, strong historical claim performance, and generally consistent repair procedures. These models are often the ones that show up as “friendly” in premium comparisons—particularly for drivers with clean records.

Readers typically notice that the lowest premiums are not always tied to the lowest market price of the car. Instead, they correlate with how insurers perceive predictability: a vehicle that insurers can forecast and service reliably. When a compact model has a reputation for fewer expensive repairs and strong crash test outcomes, underwriting becomes calmer—and calm underwriting usually means lower rates.

What to expect when comparing the lowest tier:

- Smaller premium increases after minor accidents, often due to lower repair severity.

- More stable pricing across different cities, especially where claim severity is moderate.

- Potential eligibility for discounts tied to safety tech and driver habits.

Mid-range compact car insurance costs: where trade-offs show up

Move up the ladder and the “mid-range” group appears. This is where compact car insurance becomes more nuanced. Two vehicles can have similar safety features yet different premium profiles because of differences in how often they’re involved in claims, the cost of specific components, or regional variability.

Mid-range pricing commonly reflects a blend of strengths and friction points. A compact car might be relatively affordable to insure overall, yet certain trims—especially those with high-value wheels, advanced lighting packages, or sport-oriented body kits—can increase repair costs. Likewise, a model might be popular among new drivers, nudging claim frequency upward even if severity stays reasonable.

Common reader-friendly details in this band: you’ll often see a wider spread between liability-only and full coverage. You may also notice that comprehensive claims (theft, vandalism, weather) can behave differently than collision claims. Some compact cars are statistically less likely to be stolen but more likely to suffer windshield damage; others show the opposite pattern.

Higher-cost compact car insurance: the “expensive-to-repair” territory

The upper end of compact car insurance costs often involves vehicles that are costlier to repair or more likely to be part of larger claims. This doesn’t necessarily mean the cars are unsafe. It often means the parts are pricier, the repair process is more labor-intensive, or the vehicle has a higher likelihood of being involved in incidents that produce substantial damage.

Premiums can also climb when a compact model is equipped with sophisticated technology that increases replacement costs. Sensors, cameras, and advanced driver-assistance components may require recalibration after certain types of repair. If a vehicle’s structural elements or body panels are more complex, a seemingly minor bump can become a multi-step repair job.

What makes premiums feel higher here:

- Full coverage can spike because comprehensive and collision payouts are costlier on average.

- Repair networks may handle the car differently by region, affecting labor rates and parts availability.

- Aftermarket parts compatibility can vary, influencing insurer expectations for quality restoration.

Why coverage type reshapes the lowest-to-highest ranking

Readers often assume that ranking by insurance cost is universal. In practice, it depends on what coverage is being compared. Liability-only policies typically show smaller differences because they involve legal responsibility rather than direct vehicle repair costs. Full coverage policies tend to reveal the true “car effect” because the premium must anticipate damage to the vehicle itself.

For compact cars, this means comprehensive and collision can reorder the ladder. A model might be inexpensive to insure for liability, yet expensive when the focus shifts to glass, body panels, or theft exposure. Another compact could be average in collision costs but high in comprehensive pricing due to susceptibility to certain weather-driven claims.

Regional pricing: compact premiums are local, not theoretical

Even the best compact-car insurance comparisons can mislead if they ignore location. Garaging addresses strongly influence rates: urban areas tend to have more traffic density and higher claim frequencies, while regions with severe weather can raise comprehensive costs through hail, flooding, and storm damage.

If you’re scanning premiums “lowest to highest,” expect regional variation to create a second ladder. A compact model that looks economical in one state can move upward in another if theft or repair labor costs are higher. In some places, the same vehicle might attract a different rate because insurer loss models are calibrated to local claim realities.

Trim levels, deductibles, and driver details: the invisible multipliers

Two drivers shopping the same compact model can still receive different quotes due to deductibles and personal factors. A higher deductible may reduce premium cost, but it shifts more financial responsibility to the driver when a claim occurs. That trade-off can substantially affect the “effective” ranking—especially for drivers who rarely file claims.

Trim levels matter, too. Higher trims often bring larger wheels, panoramic features, or premium lighting systems. Those elements can inflate replacement costs and can also slightly alter theft desirability. Meanwhile, driver details—age, credit-based insurance scoring where permitted, driving record, mileage estimates, and coverage history—can either suppress or amplify the vehicle’s baseline risk.

How readers can compare compact insurance costs without getting lost

The easiest way to avoid comparison confusion is to standardize the inputs. When evaluating “lowest to highest,” readers should compare the same coverage limits, deductible amounts, and policy add-ons. Otherwise, it’s like ranking athletes using different rules.

Look for:

- Consistent deductibles across quotes.

- Comparable liability limits so legal responsibility is measured the same way.

- Same full coverage structure (comprehensive + collision) to avoid mixing liability-only comparisons with full coverage conclusions.

- Discount alignment such as multi-policy bundling, safe-driver programs, and vehicle safety feature credits.

Finally, remember that insurance is not a static price tag. Premiums evolve with new model years, repair trends, and shifting claim behavior. A compact that looks “high” today could moderate later if insurers update repair cost models or if safety tech becomes more widespread.

Conclusion: choosing a compact with confidence

Compact car insurance costs—from lowest to highest—are shaped by more than brand names and sticker prices. They reflect a dynamic interplay of vehicle engineering, repair complexity, claim patterns, and local risk conditions. When readers understand the spectrum—lowest-cost insurables, mid-range trade-offs, and higher-cost repair realities—they can compare models with sharper clarity.

The best outcome is not simply finding the lowest number on a quote sheet. It’s finding the right balance: a compact car whose insurance profile fits your budget today and whose long-term coverage costs feel manageable tomorrow. With standardized comparisons and attention to coverage type, deductibles, and regional factors, the “ladder” becomes a tool rather than a mystery.