Choosing a family car in 2025 is no longer just about safety ratings and cargo space. In kitchen-table budgeting, insurance costs can quietly become the largest monthly variable. The numbers matter, but so does context: trim level, driver profile, parking conditions, collision frequency in your area, and even the way a vehicle’s repair ecosystem is priced. Below is a practical, reader-friendly tour of the cheapest 2025 family cars to insure, anchored in the same kinds of insurance institute indicators used when analysts compare model-year risk.

Expect this guide to move like a conversation—clear, sometimes granular, and always tied to what families actually experience: school runs, road trips, winter commutes, and the occasional fender-bender in a crowded lot.

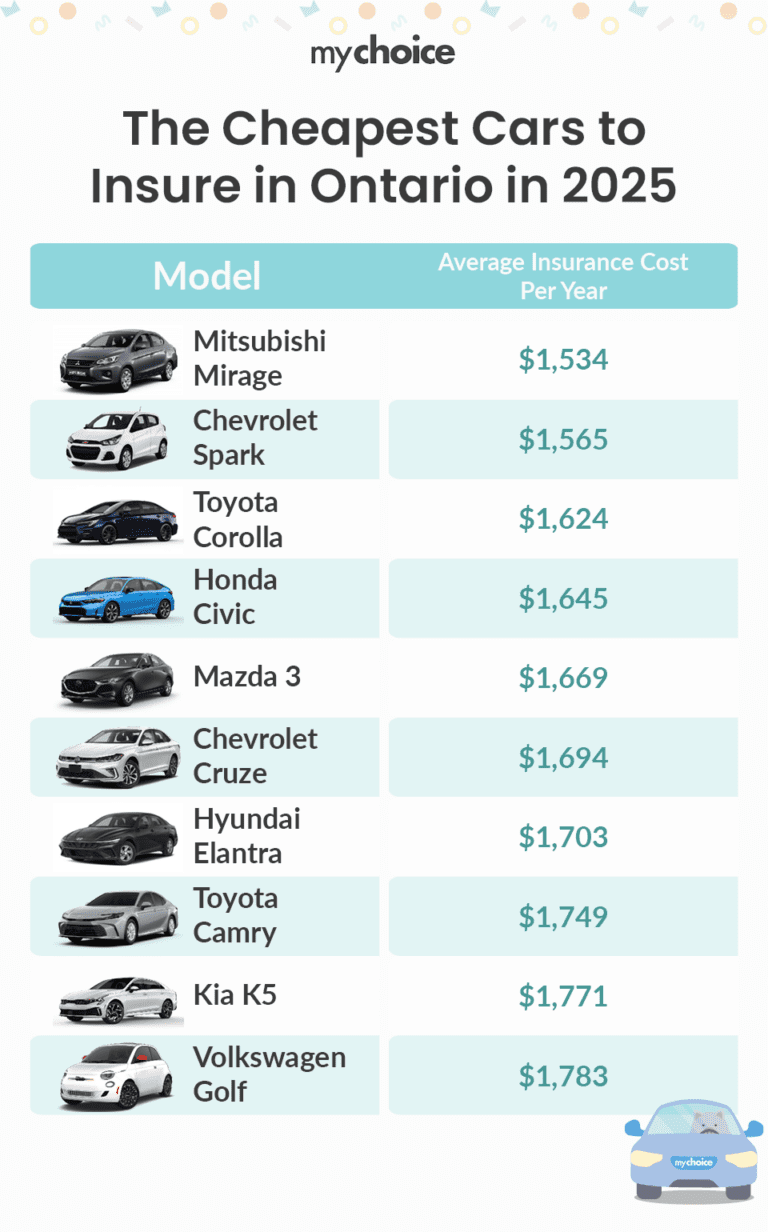

What “cheapest to insure” really means in 2025

“Cheapest” is not a single magic number. It’s a pattern emerging from multiple inputs: claim frequency, severity, theft exposure, parts availability, and how difficult repairs tend to be. A car can be inexpensive to insure because it’s less likely to be involved in incidents, or because the typical claim is cheaper to settle. In some cases, both forces are at work.

Insurance institutes frequently normalize these comparisons so they don’t merely reward the most common vehicles. That’s why a less flashy family car can outperform a popular model in the “cost-to-insure” rankings. In 2025, families are also benefiting from newer pricing models that better reflect vehicle-specific repair costs and updated safety technology.

The insurance math behind family vehicles

Family cars sit at an interesting intersection of buyer preferences and insurer assumptions. A minivan or crossover may be driven more often, but they’re often equipped with advanced driver-assistance features and built on mainstream platforms—both of which can reduce claim severity.

On the other hand, insurers also evaluate how replacement parts are priced and sourced. If a vehicle uses rare components or requires specialized calibration after a collision, premiums can rise. Even paint costs can matter, especially for models with complex coatings and higher labor time.

Another quiet factor is damage patterns. Cars used for family logistics—loading groceries, child seats, and equipment—may experience more minor impacts. The cheapest-to-insure models often have a favorable balance: common repair procedures, widely available parts, and manageable labor costs.

2025’s most insurance-friendly family car types

When people ask which cars are cheapest to insure, they usually imagine a single brand and model. In reality, vehicle type influences risk pathways. Several categories tend to be insurance-friendly for families in 2025.

1) Compact sedans and “practical” small crossovers: These models often have strong parts availability and predictable repair workflows. Their crash compatibility and moderate repair complexity frequently keep premiums lower.

2) Mid-size wagons and versatile sedans: With good crash structures and commonly stocked components, they can offer an ideal blend of family space and insurer cost control.

3) Minivans: Minivans are built for daily hauling and can be less costly to insure when equipped with mainstream mechanical systems and safety features. Many insurers reward the predictable repair profiles.

4) EVs and hybrids (select cases): Some hybrids are surprisingly affordable to insure because their components and repair histories are well understood. However, outcomes vary widely depending on battery coverage, local repair capacity, and the particular model’s claim pattern.

In short: the “cheapest” family options often come from vehicles insurers can service and price confidently.

Top picks: cheapest 2025 family cars to insure (what to look for)

Rather than presenting a simplistic list, focus on the criteria that make a car likely to land on the low-premium side. In 2025, families should look for vehicles that combine the following traits:

Safety systems that reduce claims severity: Automatic emergency braking, lane assistance, and collision mitigation can lower the probability of high-cost damage.

Moderate repair complexity: Cars designed for efficient body repair and widely available parts usually carry lower insurance costs.

Strong crash test performance: Better structural outcomes can mean fewer total-loss scenarios.

Reasonable theft exposure: Insurers track theft rates and the ease of recovery. Vehicles that don’t attract the same level of theft often cost less to insure.

Common trims, predictable equipment: If you’re choosing a base or mid trim with fewer exotic features, repair costs can be more stable. That doesn’t mean you must sacrifice comfort—think of it as optimizing your risk-to-value equation.

If your household wants “cheap to insure” without feeling deprived, aim for a model that’s popular enough to have parts supply, but not so specialized that repairs become rare and expensive.

How your family profile changes the “cheapest” winner

A car that is cheap to insure for one household might not be cheap for another. Insurance pricing is intensely personal, even when vehicle data drives the baseline.

Consider these household variables:

Age and driving history: A good record lowers premiums across the board, but the relative differences between vehicles can narrow or widen.

Primary driver distance: More mileage often increases exposure. A car’s risk profile matters, but the total risk time matters too.

Parking situation: Garage parking can improve costs by reducing theft and weather exposure. A “cheap” model doesn’t stay cheap if it lives on a street with higher claim likelihood.

Household safety habits: Seatbelt compliance, defensive driving patterns, and even telematics-based discounts can influence final pricing.

Think of it like this: the vehicle sets the stage, but your family performs the story.

Trims, add-ons, and the art of cost-conscious family comfort

Families often upgrade for convenience: panoramic roofs, premium audio, advanced navigation, and convenience packages that add cost. Some features are worth it. Others can nudge premiums upward by increasing replacement part cost or adding labor time.

A strategic approach helps:

Choose trims that include core safety technology but avoid highly specialized exterior components if you’re optimizing insurance. If a feature is rare or expensive to replace—particularly body-mounted items or unique lighting assemblies—insurance costs can climb after the first accident scenario.

Also pay attention to wheel and tire packages. Larger wheels can look sharp but may affect repair and replacement costs, especially in winter conditions where curb impacts are more common.

New car vs. used car: 2025 implications for insurance

It’s tempting to assume new cars are always more expensive to insure. Not always. Newer vehicles can come with better safety systems and improved crash compatibility that reduces severity. That said, purchase price still affects repair and replacement cost, and replacement of advanced features can be costly.

For families, a middle path often appears: a slightly older certified option can sometimes deliver similar safety benefits at a lower claim replacement cost. Meanwhile, certain 2025 models may qualify for favorable risk assessments due to updated engineering and established repair patterns.

In practical terms: compare insurance quotes for the exact year, trim, and package you’d actually buy. The spreadsheet should match the driveway.

Reducing insurance costs without reducing family life

Cheapest doesn’t have to mean compromised. These tactics often help families keep premiums in check:

Bundle intelligently: When appropriate, bundling can reduce overall administrative friction.

Raise deductibles cautiously: A higher deductible can lower premiums, but only if your household has a realistic cushion for minor claim scenarios.

Maintain a clean ownership record: Avoid lapsed coverage, and keep driver history consistent.

Choose protective habits: Alarm systems and vehicle immobilizers can matter, especially in neighborhoods with higher theft rates.

Review annually: In 2025, family circumstances change. Kids grow, commutes shift, and mileage trends can turn the “most expensive” car into a “surprisingly manageable” option.

Common questions families ask before buying

Are cheaper-to-insure cars always less safe? Not necessarily. A vehicle can be lower cost because of repair economics and claim patterns, while still providing strong structural performance and active safety.

Do hybrids cost less to insure? Some do, but it varies by battery repair complexity and local service capacity. The only reliable answer is a quote tied to the exact trim.

What about minivans vs. crossovers? Both can be insurance-friendly. Minivans often benefit from predictable family-use patterns; crossovers can be inexpensive when their repair ecosystems are well established.

Should I avoid certain features? Don’t ban features categorically. Instead, evaluate which add-ons are expensive to replace and whether they increase claim severity costs.

Final thoughts: choosing a low-cost-to-insure family car in 2025

The cheapest family cars to insure in 2025 aren’t just the ones with lower sticker prices. They’re the vehicles that insurance systems can predict, repair, and settle with fewer expensive surprises. Focus on vehicle type, safety design, parts accessibility, and trim-level repair complexity—and then let your household details finalize the equation.

When you combine smart selection with annual quote review, insurance costs can stop being a monthly mystery. They become a controllable line item—one that leaves more budget for what families actually want: time, comfort, and the freedom to travel without financial turbulence.