Choosing between leasing and buying a compact car can feel like staring at two roadmaps drawn to the same destination—yet the tolls, scenery, and timing are radically different. Compact cars are often the sweet spot for urban living: they’re easier to park, nimble in traffic, and usually lighter on fuel. But when you add financing, depreciation, mileage limits, and warranty horizons into the equation, the question becomes less about “which is better” and more about “which saves more for your particular pattern of life.”

This article walks through the financial and practical realities of a compact car lease versus a purchase. Along the way, you’ll see what kinds of details readers can expect—from payment math and ownership timelines to risk analysis and negotiation tactics. The aim is clarity without sugarcoating, so you can make a decision that fits your budget, your driving habits, and your tolerance for uncertainty.

What a Compact Car Lease Really Means (Beyond the Monthly Payment)

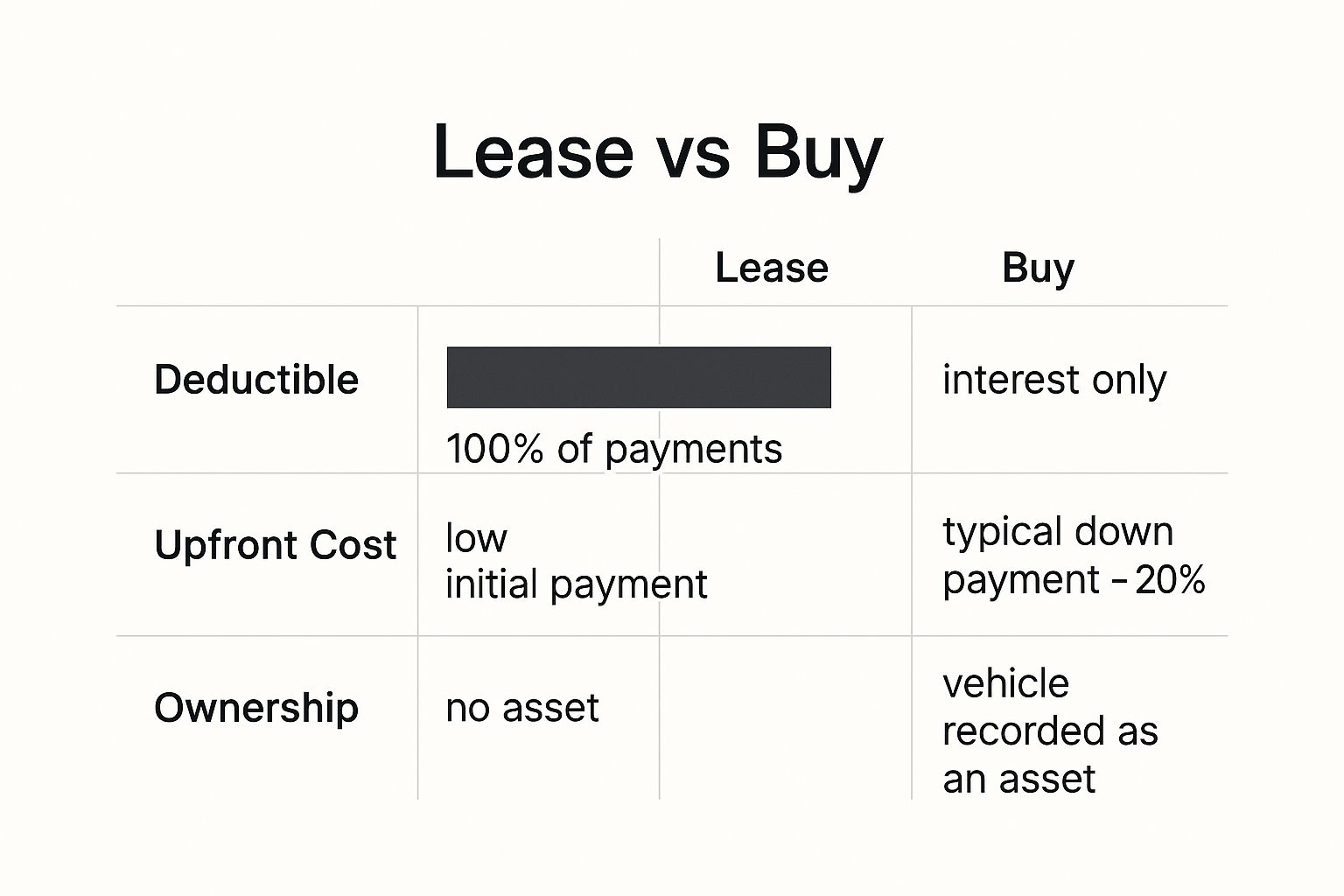

A lease is essentially a contractual “use agreement” for the vehicle during a defined term—often two to three years for mainstream compact models. You pay for the portion of the car’s value you consume during the lease period, plus financing charges and fees. That’s why lease payments can look lower than loan payments; you’re not paying for the entire vehicle to be yours at the end.

However, leasing is a precision instrument. The contract typically includes a mileage allowance and rules about wear-and-tear. Exceed those boundaries and costs can appear like stage fog—easy to ignore until they become unavoidable. Common examples include per-mile charges for high mileage and extra costs for upholstery, tires, or body damage beyond “normal” wear.

Readers should expect to evaluate:

• Lease term length and how it aligns with their future plans

• Expected annual mileage and whether it stays within the contract band

• Disposition fees and buyout options at lease end

• The “shadow costs” of wear, tires, and excess miles

What Buying a Compact Car Actually Costs Over Time

Buying is a different rhythm. With a purchase, you finance the full vehicle price (minus any down payment) and then you own the asset once the loan is paid off. In the early years, the payment may feel heavier than leasing. Yet the long arc matters: after you’ve paid down principal, your monthly obligation often shrinks dramatically compared with continuing lease cycles.

The central financial driver in buying is depreciation, which you cannot eliminate—but you can manage. Typically, compact cars depreciate most sharply in the first few years. That means the “cost” of buying is not just interest; it’s also how much value the car loses before you decide to sell, trade, or keep it for the long haul.

Expect the analysis to include:

• Total cost of ownership (TCO), including interest and taxes

• Resale value and trade-in estimates

• Repair and maintenance patterns once the warranty matures

• How long you plan to keep the car (the time horizon is everything)

Payment Comparisons: Why Leases Often Look Cheaper—At First

Monthly payment comparisons can be deceiving because they compare different endpoints. A lease payment usually funds vehicle use plus financing. A loan payment funds ownership plus financing. The difference in endpoints creates an illusion of affordability.

To compare “savings,” you need a like-for-like model. For example, consider what happens if you lease for three years and then lease again. That is a rolling sequence. Meanwhile, purchasing creates a single asset with a declining payment profile as the loan amortizes. Over several cycles, the payment picture can flip.

To make the decision more precise, readers should track these variables:

• Down payment or due-at-signing differences

• Fees (acquisition, disposition, documentation, and early termination)

• Lease interest factors versus loan APR

• The effective cost per mile (not just monthly dollars)

Mileage and Usage: The Hidden Gatekeeper of Compact Car Leases

Mileage is the lease’s gatekeeper. If you have a predictable commute and modest weekend trips, leasing can be graceful. But if your job involves variable travel, deliveries, or frequent road trips, mileage overages can dilute any apparent savings.

In financial terms, lease contracts price future uncertainty into the agreement. When your real-world driving deviates from the contract, the economics reprice themselves sharply. Buying does not have mileage penalties in the same way, though higher mileage often correlates with higher maintenance costs and lower resale value.

Readers can expect guidance on:

• Translating daily driving into annual mileage

• Estimating real-world wear patterns (tires, brakes, suspension)

• Comparing per-mile lease overages with the cost of reduced resale value in purchase scenarios

Depreciation: The Core Physics of “Which Saves More?”

Depreciation is the central engine behind both options. Leasing transfers depreciation risk partially to the lessee, but the risk isn’t uniform. The lease assumes a residual value—an estimate of the car’s worth at the end of the term. If the market value lands close to that residual, leasing can be economical. If the market turns unfavorable, the buyout calculation, disposition fees, and potential end-of-lease costs can become meaningful.

Buying also faces depreciation, but you hold the vehicle’s equity. If the resale market for your specific compact model stays strong—perhaps due to supply constraints or demand for practical fuel efficiency—your purchase can outperform the lease by a margin that feels almost serendipitous.

To approach this confidently, consider:

• Market volatility in used compact cars

• Model popularity and trim desirability

• Vehicle condition’s impact on resale premiums

• How repair receipts and maintenance history influence buyer confidence

Interest Rates and Financing: The Timing Advantage or Disadvantage

Financing rates shape both strategies, but they manifest differently. In purchases, interest accrues on the loan principal over time. In leases, financing charges are embedded into the lease structure. If borrowing costs rise, lease and buy offers both react—but the magnitude of impact can differ by program and incentive structure.

Readers should examine:

• The APR on loans versus the lease’s money factor equivalent

• Incentives or rebates that apply only to buying or leasing

• Whether a down payment is strategically wise or financially redundant

Short sentence pause: A down payment is not always an advantage.

In many cases, keeping cash for flexibility can be smarter than surrendering it upfront—especially when comparing opportunity cost against the interest rate you’re paying.

Long-Term Ownership: The “After the Warranty” Equation

Leases often end around the period when warranties are still fresh. That’s a comfort feature. Buying may extend beyond the coverage window, where repairs can become more unpredictable. Compact cars are not exotic machines, but wear items—brakes, tires, filters, suspension components—add up. When warranty coverage fades, the cost curve can climb.

Still, buying has a compensating benefit: you can plan for expenses and stop cycling into new payments. If you keep the car longer, the depreciation cost is spread over more time, and the total cost can stabilize.

This is where readers can expect a “timeline view,” often visualized as cost-per-year or cost-per-mile. The winning option depends on your patience. Some people prefer the novelty of recurring leases. Others prefer the slow, steady compounding of ownership.

Risk Management: Wear, Repairs, and Contractual Gotchas

Leasing is contractual. Buying is relational—you negotiate with mechanics, parts availability, and your own maintenance behavior. Leases charge for excess wear and require specific return conditions. If your lifestyle is rough-and-ready—kids, pets, gravel roads, or frequent hauling—those charges can become a recurring tax.

Buying has risks too: repairs may arrive without warning, and the bill can be substantial. Yet ownership gives you latitude. You can choose when to repair, what parts to use, and how to budget. That autonomy can be valuable for long-term savings, especially when you’re skilled at maintenance or have a trustworthy service partner.

Readers should look for practical guidance on documenting vehicle condition, keeping service records, and understanding what counts as “normal” wear in lease return policies.

Negotiation Tactics: How to Reduce the Cost of Either Choice

Deals are rarely just luck. They are the result of disciplined negotiation. For leasing, the focus should be on the cap cost, the residual value assumptions, and the fees. Ask pointed questions. Request an itemized breakdown. Verify whether incentives apply and whether they’re already reflected in the advertised offer.

For buying, negotiate the purchase price and the financing terms separately when possible. Consider pre-approval to reduce friction. Compare total interest over the intended term rather than the monthly figure alone.

Which Saves More: A Decision Framework for Real People

There isn’t one universal answer. Leasing tends to win when you value lower upfront cash outlay, prefer a predictable short-term budget, stay within mileage allowances, and like swapping vehicles frequently. Buying tends to win when you plan to keep the car longer, want freedom from mileage constraints, anticipate stable maintenance costs, and can tolerate higher early payments in exchange for eventual equity.

A simple framework can make the choice feel almost mechanical:

• If your time horizon is short and your mileage is controlled, leasing often saves more.

• If your time horizon is long and your mileage is uncertain or high, buying often saves more.

• If you drive fewer miles than average and prioritize novelty, leasing can be a rational choice.

• If you drive more than average and plan to keep the car, buying typically delivers better value.

Then apply sensitivity analysis. Recalculate the “savings” under different mileage assumptions, resale value ranges, and maintenance estimates. This removes bravado from the decision and replaces it with evidence.

Conclusion: The Truest Shortcut Is Matching the Vehicle to Your Life

Compact car leasing versus buying is not merely a financial contest—it’s a negotiation with your future schedule, your driving patterns, and your tolerance for contractual constraints. Leasing can feel like a clean, streamlined arrangement, especially when your mileage stays disciplined and you enjoy periodic upgrades. Buying can feel heavier at first, but ownership often grants a quieter kind of value: the long runway where depreciation spreads out and monthly burdens ease.

When the question is “Which saves more?”, the most effective strategy is to compare total costs over your actual intended ownership length, not a generic timeline. Gather the figures, model the mileage, and evaluate the risk of wear and resale. Then choose the option that aligns with how you truly drive. In the end, the best savings plan is the one you can live with—calmly—until the next decision arrives.