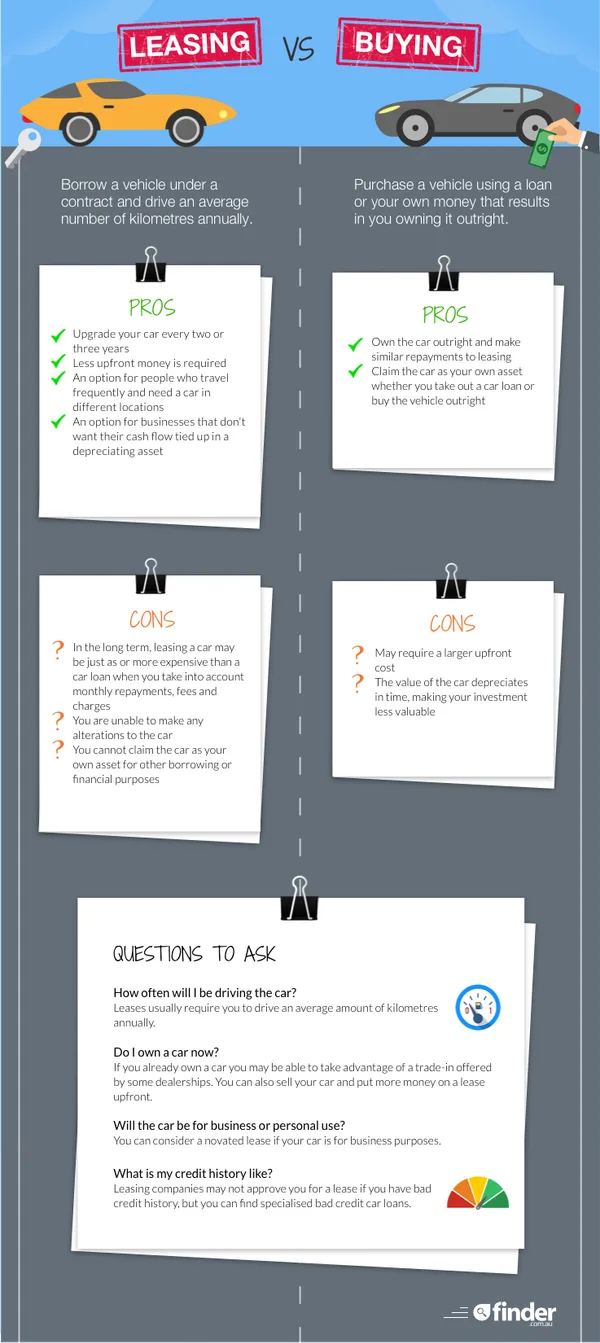

Buying or leasing a crossover is one of those decisions that looks deceptively simple—until you total up the numbers, account for depreciation, and factor in how you actually drive. A crossover can be a practical nest for commuting, weekend errands, and the occasional road trip. But whether you should lease or buy depends on more than monthly payments. The real question is: which option protects your wallet when the novelty fades and the spreadsheets wake up?

This guide breaks down the money mechanics of crossover leasing versus buying, including how different ownership timelines, mileage habits, maintenance expectations, and end-of-term options can tilt the outcome. Along the way, you’ll see what readers typically look for—clear comparisons, “what-if” scenarios, and decision frameworks—so you can match the choice to your lifestyle rather than someone else’s.

The Money Myth: Monthly Payment vs Total Cost

Leasing advertising often tempts shoppers with low monthly figures. Buying can look expensive by comparison, especially when down payments and loan terms enter the conversation. Yet monthly cost is only a slice of the pie.

For a true comparison, track the total cost of ownership over your planned horizon. For some people, that horizon is three years. For others, it’s seven. If you keep a crossover longer, buying frequently gains an advantage because depreciation runs its course and you build equity. If you trade frequently, leasing can feel like a controlled rotation of expenses.

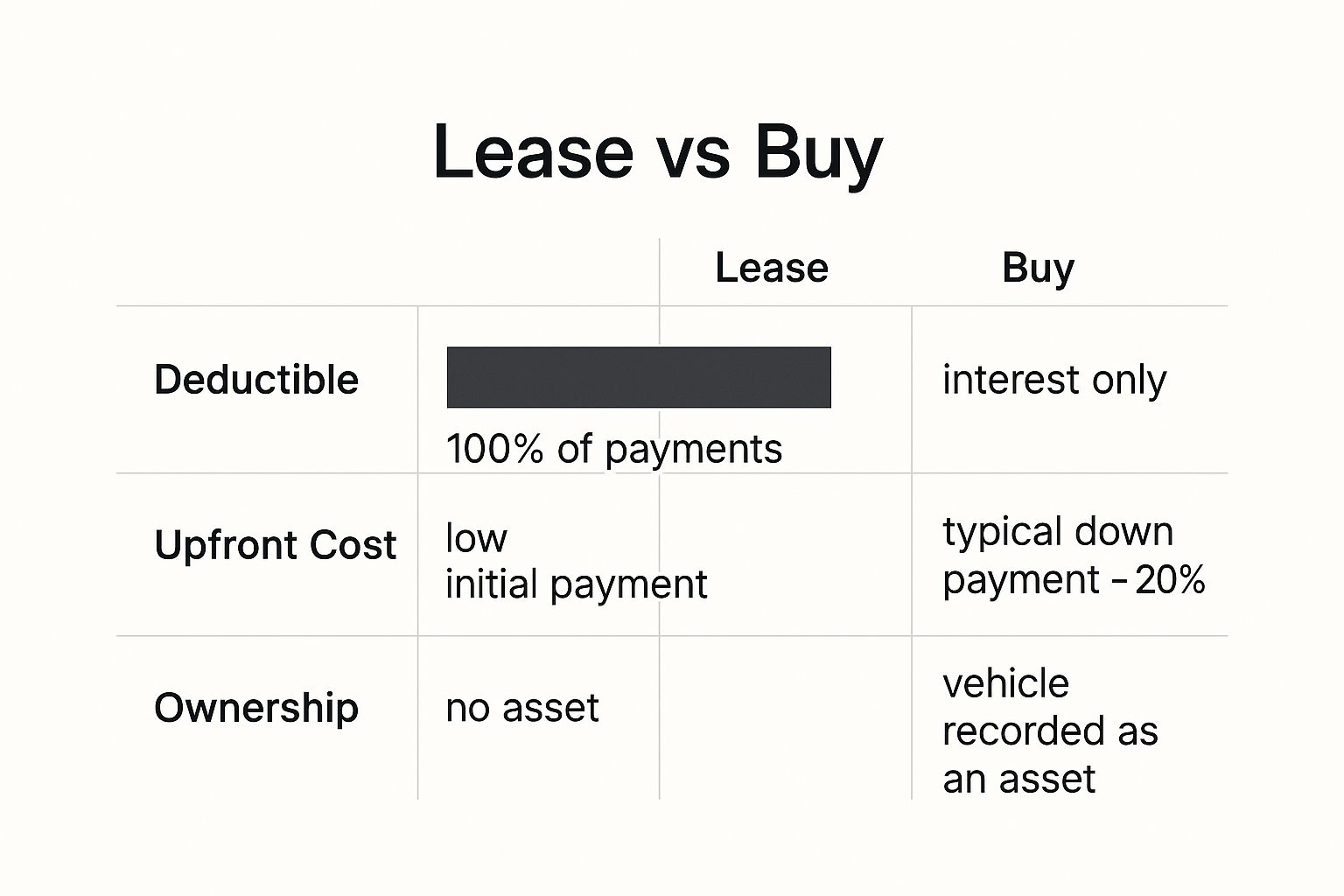

Consider the structure of costs:

Leasing often bundles depreciation and finance charges into predictable payments, while charging for excess mileage and wear-and-tear at return. Buying includes interest, taxes, insurance, and eventual depreciation, but you keep the asset after the loan is paid.

What readers can expect here is a “payment-to-economics translation.” You’ll see why two vehicles with identical stickers can diverge dramatically once time and usage are accounted for.

Depreciation: The Hidden Lever in Every Crossover

Depreciation is the silent engine behind the lease vs buy equation. Crossovers tend to depreciate quickly in the first few years. Leasing basically charges you for the portion of that depreciation you’ll experience during the lease term. Buying exposes you to depreciation across whatever years you hold the vehicle.

The key difference is perspective:

With a lease, the lender estimates future value (often called the residual). If the market value at the end is lower than expected, you may pay extra depending on the contract terms and any adjustments. If it’s higher, the lender still keeps the benefit because you’re not buying the asset.

With a purchase, depreciation is your risk and your reward. If you later sell when the market surprises upward, you can recoup more than you’d expect. If it drops, resale value becomes painful.

Readers often look for practical signals: how brand reputation, trim popularity, and mileage norms can influence depreciation. A crossover that holds demand—because of reliability, safety features, or niche utility—can make buying more financially forgiving.

Scenario Planning: Short-Term Drivers vs Long-Term Keepers

To decide, many people begin by asking a simple question: How long will I keep it?

If your life suggests mobility—job changes, expanding family needs, or a preference for newer tech—leasing can align with your rhythm. You trade predictably, and the vehicle’s early life depreciation is mostly “leased away.”

If you tend to keep cars past the point where warranties expire, buying often converts into a more cost-effective long-haul strategy. Once the loan is paid, your monthly outlay can shrink substantially. That doesn’t mean costs disappear; tires, brakes, and routine repairs will still arrive. But the “payment gravity” eases.

Expect content like this to include decision tables and timeline comparisons: 24–36 months versus 60–84 months, paired with how mileage and condition affect financial outcomes.

Mileage and the Usage Tax: Where Leases Get Sharp Edges

Leases are not inherently “bad”—they’re structured. But structure can become a trap if your driving doesn’t match the lease contract.

Most leases include a mileage cap, commonly expressed as miles per year. Exceed that cap and you may pay a per-mile charge at the end. That cost can turn what seemed like a low payment into an unexpectedly expensive mile.

Buying tends to be more forgiving for high-mileage drivers. There may still be resale depreciation, but you’re not paying a penalty for each additional mile. You’re simply living with the natural consequence of wear and usage.

Readers can expect guidance on “mileage fit”—how to estimate annual driving, anticipate life changes, and decide whether the lease mileage cap is likely to feel like a leash or a cushion.

Down Payments, Incentives, and the Art of the Deal

Deal incentives can swing the economics substantially. Lease offers might include low money factors, waived fees, or manufacturer incentives. Buying offers might include promotional APR, trade-in boosts, or cash rebates.

However, be cautious with large down payments on a lease. If the vehicle is totaled or stolen early, the down payment may not fully protect you financially. With buying, a down payment simply reduces the amount financed, often making the math more straightforward.

This is where detailed readers want transparency: how fees, taxes, acquisition costs, and documentation charges affect the true price. Even small charges can compound over time.

Expect a thorough breakdown of negotiating levers: price of the vehicle (negotiable in most contexts), residual value assumptions (lease-specific), and financing terms.

Wear-and-Tear vs Real-World Ownership

Leases often treat vehicle condition like a bank account. Excess wear—scratches, dents, or interior damage—may be assessed at return time. Tires and brake condition can also matter depending on the policy.

Buying shifts responsibility differently. You’ll pay for repairs, but you’re not typically subject to a predetermined return inspection that can generate surprise deductions. Still, repairs are real money, and ignoring them can reduce resale value.

Many readers prefer a “reality check” section: how to maintain a crossover to reduce risk under a lease, and how to budget repairs proactively if you buy.

Think of it as the contrast between predictable penalties (lease return) and variable maintenance (ownership).

Maintenance, Repairs, and the Warranty Horizon

Leasing often coincides with warranty coverage, especially during the first few years of ownership. That can reduce out-of-pocket repair exposure. But warranties don’t cover everything, and wear items still have limits.

Buying can offer comparable peace of mind if you purchase within a warranty window. Yet the longer you keep a vehicle, the more you’ll feel the approach of “out-of-warranty costs.” That’s when an emergency fund becomes as important as the interest rate.

Readers usually appreciate a breakdown of common crossover expenses: tires, brakes, battery health, and suspension components. The financial question is not whether maintenance exists—it’s how you plan for it.

Equity and the Resale Reality

Owning builds equity. Even if the equity grows slowly at first, it becomes a tangible asset once the loan balance declines. Equity matters when you sell, trade in, or even refinance.

Leasing doesn’t build ownership equity. The value is “captured” by the leasing company. Your payoff comes from driving a newer vehicle without long-term ownership commitments.

Some readers want a nuanced perspective: a lease can still be sensible if your goal is to avoid risk around resale. Buying can be more attractive if you understand resale patterns and plan to sell strategically.

Insurance, Taxes, and Other Costs That Sneak In

Insurance premiums may vary by lender requirements on leased vehicles and by your driving record. Taxes depend on local regulations and the way the payment is structured. Registration and licensing can be similar, but not always.

The practical takeaway is to treat these line items as non-negotiable inputs. A small tax difference can matter over three years. A lender-driven insurance requirement can change your monthly budget.

Expect readers to want “all-in” calculators and checklists that prevent the classic mistake: comparing only the sticker and the monthly payment.

So Which Saves You Money? A Decision Framework

If your schedule is stable, mileage is predictable, and you plan to keep a crossover for several years, buying can often yield better financial outcomes. You pay interest and absorb depreciation, but you end with a vehicle you can sell or keep—without ongoing lease commitments.

If you prefer frequent upgrades, want predictable payments, and can live within the mileage and condition parameters, leasing can be a cost-efficient form of convenience. It’s often strongest when your planned ownership duration matches the lease term and when you maintain the vehicle carefully.

The most money-smart approach is to run three scenarios: a best-case lease, a realistic lease, and a long-term buy. Use your expected annual mileage, estimate how long you’ll keep the crossover, and include fees, taxes, maintenance, and any likely end-of-term costs.

Final Thoughts: Matching the Vehicle to Your Budget Personality

Choosing between a crossover lease and buy is less about ideology and more about alignment. Leasing can feel like renting freedom with a clear end date. Buying can feel like investing in mobility with a longer payoff horizon. Neither is universally cheaper; the numbers become obvious only when they’re matched to your actual driving, timeline, and tolerance for risk.

If you want the most economical outcome, build a full-cost picture, not a payment snapshot. Then choose the option that fits how your life moves—because the best deal is the one that stays favorable even when the calendar and the odometer don’t cooperate.